Prices for Flexible Packaging materials have passed their peak but remain above their long-term trends

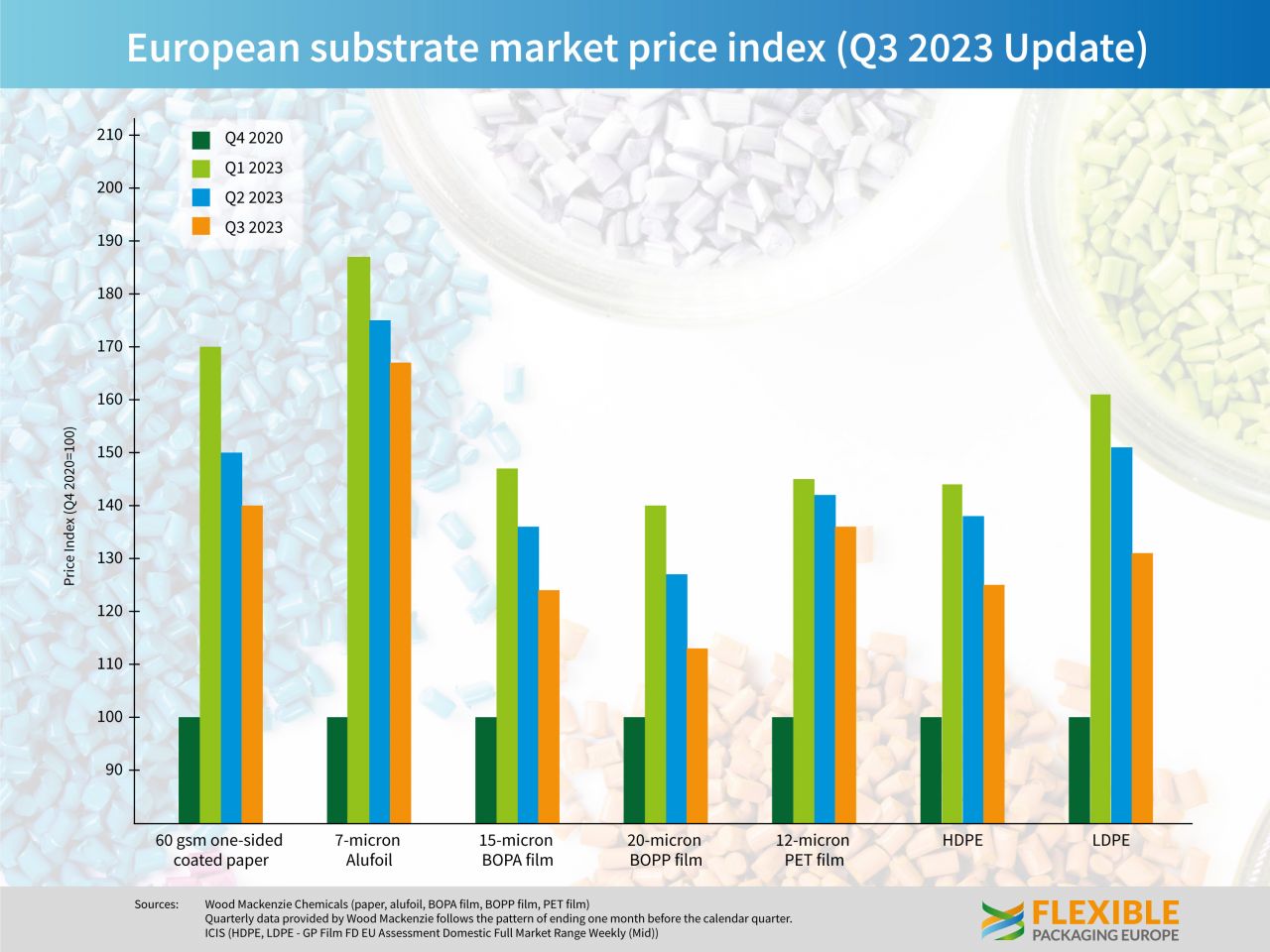

Having peaked midway through 2022 the basket of flexible packaging materials used to measure price levels have continued to decline in Q3 2023, following the trend seen in the first half of the year. While they are all still above the benchmark price set in Q4 2020 (100%) most have dropped by about 10% to 20% since the previous quarter, according to figures recently released by Flexible Packaging Europe (FPE).

HDPE and LDPE prices declined 10% and 14% respectively vs. Q2 2023 to end Q3 at 125% and 131% compared to Q4 2020. Sixty gsm one sided coated paper fell 7% and is now at 140%, while BOPA 15-micron film shed 8% to stand at 124% and BOPP 20-micron film dropped 11% and is now at 113%, the closest to the original benchmark price. PET 12-micron film fell just 4% in the last quarter and now stands at 136%.

David Buckby, senior analyst at Wood Mackenzie added some context to the latest figures, “Across the grades of film, foil and paper that we track, prices paid in Europe for flexible packaging materials decreased in Q3, as was the case in Q2. Price declines are being driven by continued weakness in order volumes, a function of poor European consumer demand and destocking. In addition, certain substrate markets are in a state of global overcapacity, following sharp increases in the amount of production capacity over the past few years.”

“Looking ahead, while we believe some substrate prices will continue to decline in Q4, there is a possibility of more stability for certain products,” he added.

Guido Aufdenkamp, Executive Director of FPE, believes the outlook remains uncertain, “The combination of end-consumers reluctance to purchase packaged foods and remaining stocks along the value chain is still affecting the demand for flexible packaging in the short-term. Overall inflation is dropping, but not as quickly as some anticipated. It must be remembered that while these, mostly double digit, declines are to be welcomed to outbalance the inflation, the price basket of flexible materials is still much higher than pre-Covid levels and continues being volatile. For all these reasons our customers remain very cautious, as do the material suppliers, but we anticipate demand will pick up through 2024.”

*All comparisons are with Q4 2020 as a base at 100%.

{kind=link}