Flexible packaging materials: Geopolitical tensions drive significant raw material price increases in the second quarter of 2026

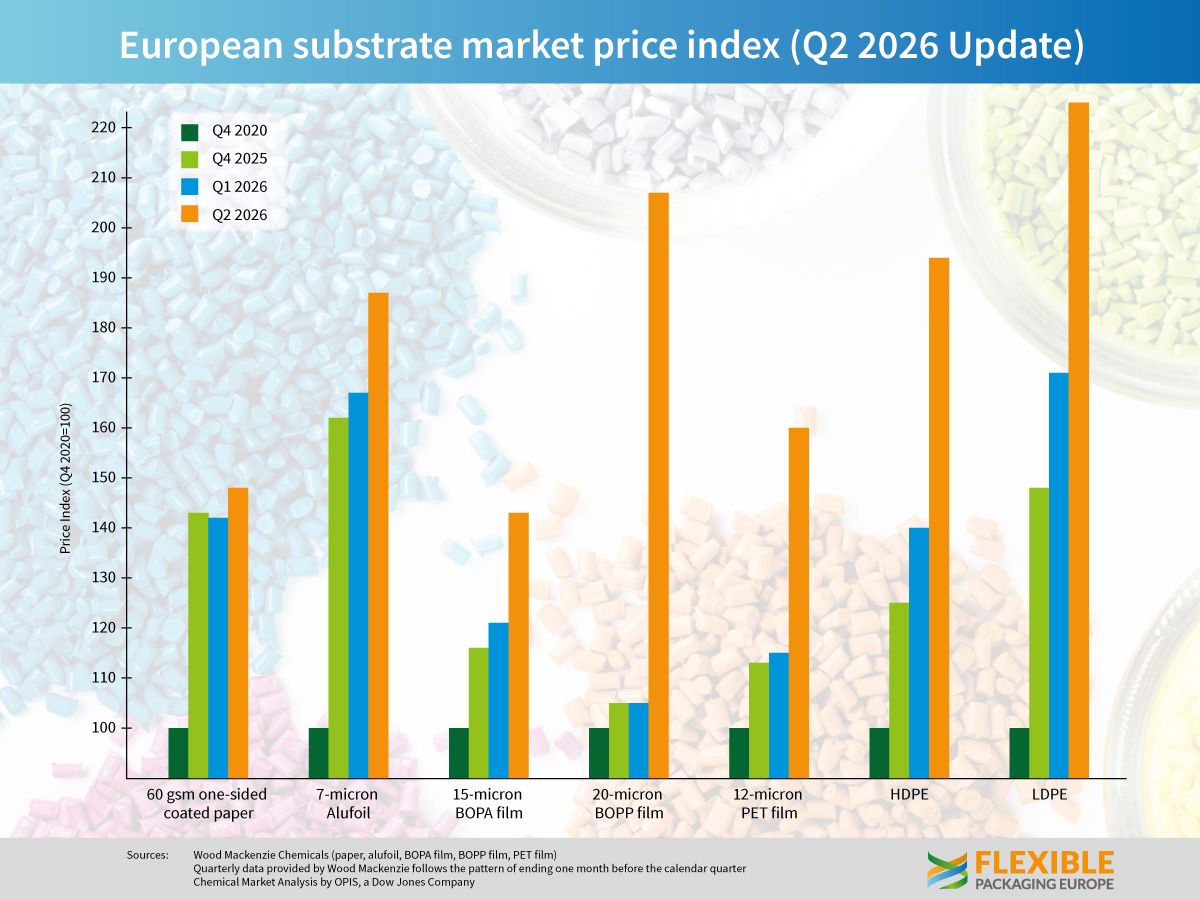

Markets for flexible packaging materials recorded substantial price increases during the second quarter of 2026. According to the FPE Raw Material Price Index, quarterly minimum prices rose significantly across all substrates compared with the previous quarter.

The most pronounced increase was seen in BOPP film (20 micron), where price levels almost doubled (+97%) compared with the first quarter. PET film (12 micron) also increased sharply by around 40%, while BOPA film (15 micron) rose by 21%. Aluminium foil (7 micron) became approximately 12% more expensive, while one-side coated paper (60 gsm) increased by just under 5%. Polyethylene markets also experienced strong price increases, with average price levels for HDPE rising by around 38% and LDPE by around 31% compared with the previous quarter. Compared with the second quarter of 2025, all materials monitored were trading well above their year-earlier levels.

Alexander Tkachenko, Wood Mackenzie, commented: "BOPET prices increased by an average of €0.55/kg during the quarter, driven by rising oil prices and concerns over potential PTA and MEG supply shortages. BOPP prices have nearly doubled over the same period, primarily due to a very tight PP resin supply in Europe, as inventories were already low before the onset of the conflict. BOPA film prices have also risen significantly, supported by increases in the costs of PA6, PA66 and caprolactam. Aluminium foil prices increased by €0.62/kg this quarter as a result of higher LME prices and substantially increased warehouse premiums. Paper prices rose by €0.06/kg; while paper is less directly affected by petrochemical market dynamics, sustained high oil and energy prices through the winter could lead to delayed cost increases driven by higher energy costs."

Polyethylene markets were also significantly influenced by geopolitical developments during the second quarter.

Kaushik Mitra, Chemical Market Analytics by OPIS, a Dow Jones Company, said: "The European polyethylene market experienced significant volatility during the second quarter of 2026, driven by the Iran crisis and the prospect of a supply shock in a market already characterised by low inventory levels. After remaining at relatively low levels from the second half of 2025 until February 2026, polyethylene prices in Europe rose sharply in March. This trend continued throughout April and May as buyers prioritised material availability. Supply remained tight due to the significant displacement of production from the Middle East, while other international suppliers required time to reconfigure their trade flows. Although European production gradually increased, incoming orders continued to exceed available supply. Prices plateaued in May as buyers shifted their focus from material availability to affordability following restocking, while prices in Asia had already begun to reverse. Increasingly competitive offers, particularly from China, strengthened buyers' negotiating position. From the second half of May onwards, spot market prices began to ease, raising concerns over inventory devaluation and dampening purchasing activity. Although spot prices continued to decline during June, they remained above pre-crisis levels. The prospect of a potential peace agreement between the United States and Iran is already weighing on crude oil and feedstock prices. The reopening of the Strait of Hormuz is expected to ease supply chain bottlenecks and contribute to a normalisation of supply in Europe. Historical experience and statistical correlations indicate that lower feedstock prices generally result in lower polyethylene prices, provided that supply constraints do not become a limiting factor."

Developments during the second quarter highlight the strong dependence of European raw material and packaging markets on geopolitical events and global trade flows. At the same time, the recent decline in polyethylene market prices, together with expectations of improving supply conditions, points to the first signs of a potential market stabilisation during the second half of the year.

"The second quarter of 2026 was characterised by exceptional price increases across almost all key packaging substrates," summarised Guido Aufdemkamp, Executive Director of Flexible Packaging Europe (FPE). "These developments were primarily driven by geopolitical supply risks, rising energy and raw material costs, and considerable uncertainty across global supply chains. However, the European suppliers of flexible packaging could generally deliver all volumes requested and will continue doing so. Overall, the volume market outlook is cautiously optimistic for the rest of the year assuming stabilisation of the geopolitical situation. The industry is concerned about the general private consumption impacted by upcoming food inflation.”

{kind=link}